New exemptions on stamp duty and real property gains tax to boost Malaysian property market

The momentum of economic growth in Malaysia has weakened considerably due to the outbreak of the COVID-19 pandemic. In its continuing efforts to save Malaysia from the pandemic-induced economic fallout, the Government has, on 5 June 2020, unveiled Pelan Jana Semula Ekonomi Negara or the National Economic Recovery Plan (PENJANA) [link here] which contains 40 initiatives strategically designed to propel the nation’s economic growth.

To boost the Real Estate sector, PENJANA unveiled the following initiatives:

- reintroducing the Home Ownership Campaign (“HOC”):

- by granting stamp duty exemption on instruments of transfer and loan agreements for acquisitions of residential properties priced between RM300,000 and RM2.5 million. The exemption on any instrument of transfer is limited to the first RM1 million of the value of the residential property while full stamp duty exemption is given on the loan agreement; and

- introducing the Real Property Gains Tax exemption.

In connection with these initiatives, the following legislation were gazetted on 28 July 2020 with retrospective effect from 1 June 2020.

A. Stamp Duty Exemption (No. 3) Order 2020

Stamp duty shall be exempted in respect of any “loan agreement” to finance the purchase of residential property under the HOC. Such exemption will be given, subject to the following conditions:

- the sale and purchase agreement (“SPA”) was executed on or after 1 June 2020 and not later than 31 May 2021 and is stamped at any branch of the Inland Revenue Board Malaysia (“IRB”), subject to the condition that developers provide at least 10% discount from the original price except for a residential property which is subject to controlled pricing; and

- the SPA is made between an individual and a property developer who is registered with the Real Estate and Housing Developers’ Association (“REHDA”) Malaysia, Sabah Housing and Real Estate Developers Association (“SHAREDA”) or Sarawak Housing and Real Estate Developers’ Association (“SHEDA”).

| Instruments on Securing Loan | ||

| Loan Amount | Stamp Duty | Stamp Duty Under HOC 2020-2021 |

| Up to RM2,250,000 | 0.5% | Exempted |

A copy of the Order can be found here.

B. Stamp Duty Exemption (No. 4) Order 2020

Stamp duty shall be exempted on the “instrument of transfer” for the purchase of a residential property under the HOC. Such exemption will be given subject to the following conditions:

- the SPA is executed on or after 1 June 2020 and not later than 31 May 2021 and is stamped at any IRB branch, subject to the condition that developers provide at least 10% discount from the original price except for a residential property which is subject to controlled pricing; and

- the SPA is made between an individual and a property developer who is registered with the REHDA, SHAREDA or SHEDA.

| Instruments of Transfer | ||

| House Price | Stamp Duty | Stamp Duty Under HOC 2020-2021 |

| First RM100,000 | 1% | Exempted |

| RM100,001 – RM500,000 | 2% | Exempted |

| RM500,001 – RM1,000,000 | 3% | Exempted |

| RM1,000,001 – RM2,500,000 | 4% | 3% |

A copy of the Order can be found here.

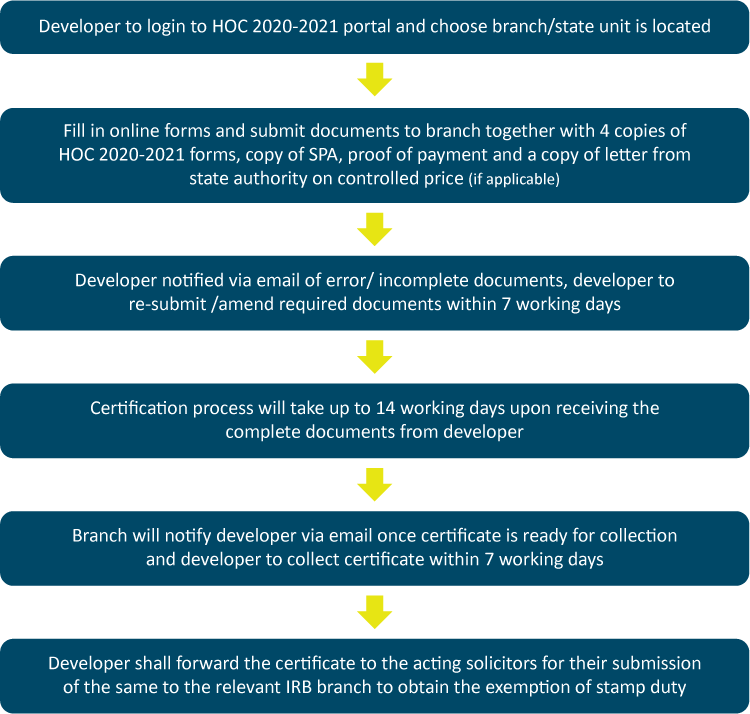

In view of the stamp duty exemption orders and subject to the fulfilment of the conditions, once the SPA has been executed, it will be stamped with the nominal stamp duty, i.e. RM10 per copy. Thereafter, the Developer shall apply for the REHDA certificate to prove the eligibility for the entitlement of exemption for both the instrument of transfer and loan agreement. The application may take approximately 14 working days. Once the application has been approved, the REHDA certificate shall be attached to the instrument of transfer and loan agreement for the purposes of obtaining the exemption of stamp duty upon submission of the same to the relevant IRB branch.

The application process is as follows:

C. Real Property Gains Tax (Exemption) Order 2020 (“Exemption Order”)

Under the Exemption Order, gains arising from disposal of residential properties after 1 June 2020 until 31 December 2021 will be exempted from Real Property Gains Tax (“RPGT”). Such exemption is granted for up to three residential properties per individual if the following conditions are fulfilled:

- the disposer must be an individual who is a Malaysian citizen and is the sole or joint owner of the property to be disposed;

- the property disposed must be a ‘residential property’, namely a house, a condominium unit, an apartment or flat in Malaysia, and includes a service apartment and a small office home office (SOHO) which is used only as a dwelling house;

- the residential property which is being disposed of is not acquired by way of:

- transfer between spouses; or

- gift between spouses, parent and child, or grandparent and grandchild where the donor is a citizen; and

- the SPA for the disposal of the residential property is executed on or after 1 June 2020 but not later than 31 December 2021 and is duly stamped not later than 31 January 2022. Where there is no SPA, the instrument of transfer for the disposal of the residential property is executed on or after 1 June 2020 but not later than 31 December 2021, and is duly stamped not later than 31 January 2022.

Where an individual disposes of more than three units of residential properties, the disposer may elect any three from the said disposals to be exempted. Once the decision is made, the election is final and irrevocable.

In the event the disposal of the residential property is a conditional contract requiring the Federal Government or a State Authority’s approval, the exemption will be applicable subject to the following conditions:

- the contract of disposal of a residential property is executed on or after 1 June 2020 but not later than 31 December 2021 and is duly stamped not later than 31 January 2022; and

- the approval is obtained on or after 1 June 2020.

Similar to the stamp duty exemptions under HOC, it appears that the RPGT Exemption is only given to Malaysian citizens. Currently, the applicable RPGT rates for Malaysian citizens and permanent residents range from 5% to 30% depending on the holding period.

A copy of the Exemption Order can be found here.

Conclusion

The initiatives introduced under the PENJANA will give the property market a well-needed boost in light of the downturn due to COVID-19. The HOC, which was initiated in 2019, is said to have cleared some RM23.2 billion worth of houses, surpassing the initial target of RM17 billion and greatly assisted developers with the overhang of completed properties. The exemption of stamp duties was useful for first time buyers keen to purchase completed properties at a discounted price. It is hoped that the reintroduction of the HOC will achieve its intention to stimulate the property market and provide financial relief to home buyers specifically, the citizens of Malaysia during this difficult time. The boost to the property sector will in turn hopefully help other industries tied to real estate development, such as construction, banking, manufacturing and furniture, and the professionals and consultants that provide services to the real estate industry.

If you have any questions or require any additional information, please contact Sunita Sothi, Farina Mohamad Yahya or the Zaid Ibrahim & Co partner you usually deal with.

This article was prepared with the help of Nanthini Marutheappan and Lim Zi Yi.

This alert is for general information only and is not a substitute for legal advice.